by Cissy Blanchard | Apr 15, 2025 | Market Commentary

Market Commentary

The first quarter of 2025 saw domestic stocks under pressure (S&P 500 down 4.3%) while international equities rallied (MSCI EAFE up 6.9%). Core bonds fared well in the face of volatility (Bloomberg U.S. Agg Bond Index up 2.8%).

2025 began with optimism in global equity markets. January saw solid gains driven by resilient U.S. economic data. Optimism around further deregulation and more favorable tax policies also contributed to rising business and consumer sentiment. In February, the tech space and specifically companies at the forefront of Artificial Intelligence were thrust into the spotlight when the emergence of DeepSeek’s AI breakthrough bolstered sentiment towards Chinese technology companies. These developments brought scrutiny towards the dominance and valuations of U.S. tech companies. Concurrently, geopolitical events unraveled with the U.S. breaking away from its longstanding approach of exerting influence through aid and defense support to many allies, leading to those countries looking to bolster their own national defenses through fiscal spending. Germany was the standout, pledging €500 billion towards a future infrastructure and defense spending package. The U.S. took a different approach, pledging to cut government spending and creating the Department of Government Efficiency (DOGE) that looked to eliminate government waste.

Throughout these very meaningful events, the Trump administration had been discussing imposing tariffs on global trading partners that were “taking advantage of the U.S.” as well as on friendlier trading partners like Mexico and Canada, where tariffs were being threatened as a way to beef up border security to combat fentanyl and other dangerous drugs coming into America. The exact goal of the tariffs and the extent to which our trading partners would be impacted were unclear, leading to uncertainty in the business and investing landscape. U.S. equities saw extreme volatility and outflows from international investors due in part to political pressure and in part due to the relatively less volatile developed international markets.

2025 has been eventful through the first 3 months and the headlines are still coming in fast. In the early days of April, we have seen a global tariff policy announced by the Trump administration that imposed significant “reciprocal” tariffs based on trade deficits leading to responses by those countries ranging from retaliatory to wanting to negotiate. Global markets have sold off in response to the higher than feared policy and an unclear path forward in the coming months. We anticipate continued market volatility in the near term as investors await further clarity on these economic policies.

Portfolio Commentary

Equity Sleeve: We continue to maintain a mix of active and passive strategies across our equity exposures. While international equities look attractive with the backdrop of lower relative valuations and potential persistence of a weakening dollar, we still favor a domestic tilt to US Stocks. We are allocating more to Value and equity funds that exhibit a defensive bias as we navigate near term policy uncertainty. Relative to broad Large Cap Equity benchmarks, we are overweight mid and small cap stocks.

Fixed Income Sleeve: Fixed Income continues to experience volatility as markets anticipate how many Fed cuts, we can expect in 2025. In the aftermath of significant inflation and a historically fast rate hiking cycle, fixed income has proven to be a helpful defensive ballast in portfolios during the tariff environment we’ve been experiencing the last few weeks. However, potential risks within credit markets and rate volatility remain. We will continue to rely on active managers to help navigate a changing rate and credit environment.

Alternatives Sleeve: To further diversify the fixed income portion of portfolios, we use a blend of diversified, balanced, and active managers designed to help navigate choppy markets. This strategy is meant to complement, not replace traditional fixed income as we aim to produce meaningful real returns while maintaining the primary focus of fixed income which is diversification from stock volatility. Included in this sleeve are strategies that use options to either reduce portfolio volatility, generate income, or both.

Securities and advisory services offered through LPL Financial, a registered investment advisor, Member FINRA/SIPC

The commentary in this report is not a complete analysis of every material fact in respect to any company, industry, or security. The opinions expressed here are not investment recommendations, but rather opinions that reflect the judgment of Horizon as of the date of the report and are subject to change without notice. Forward-looking statements cannot be guaranteed. We do not intend and will not endeavor to provide notice if or when our opinions or actions change. This document does not constitute an offer to sell or a solicitation of an offer to buy any security or product and may not be relied upon in connection with the purchase or sale of any security or device.

Equity markets are represented by the S&P 500 Index. The S&P 500 is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. The MSCI All Country World Index (ACWI) is a global equity index that tracks the performance of large- and mid-cap stocks in developed and emerging markets. The Bloomberg U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities and collateralized mortgage-backed securities. References to indices, or other measures of relative market performance over a specified period of time are provided for informational purposes only. Reference to an index does not imply that any account will achieve returns, volatility, or other results similar to that index. The composition of an index may not reflect the manner in which a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change. Indices are unmanaged and do not have fees or expense charges, both of which would lower returns. It is not possible to invest directly in an unmanaged index.

This commentary is based on public information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied on as such.

Horizon Investments and the Horizon H are registered trademarks of Horizon Investments, LLC.

© 2025 Horizon Investments

by Cissy Blanchard | Mar 20, 2025 | Financial Planning

Introduction

Artificial intelligence (AI) is no longer just a buzzword in finance—it is fundamentally reshaping the way financial institutions serve their clients. From streamlining processes to enhancing security and providing smarter insights, AI is enabling financial firms to offer more personalized, data-driven solutions.

Clients today expect efficiency, accuracy, and tailored advice. AI is making this possible by analyzing financial patterns, predicting risks, and offering proactive recommendations. While financial expertise and human judgment remain essential, AI is enhancing the capabilities of financial professionals, making wealth management more precise and efficient than ever before.

AI’s Role in Transforming Financial Services

One of the biggest shifts in finance is AI’s ability to process vast amounts of data at incredible speeds. This allows financial institutions to identify market trends, assess risks, and provide clients with deeper insights in real time. AI-driven analytics are making financial planning and investment strategies more precise, helping clients navigate changing economic landscapes with confidence.

Beyond investments, AI is also improving financial security. Fraud detection has become more sophisticated, with AI systems able to analyze transactions in real-time and flag suspicious activity before it becomes a problem. Clients benefit from an added layer of protection, reducing the risk of financial fraud and identity theft.

At the same time, AI is enhancing customer service. Intelligent virtual assistants and chatbots are streamlining client interactions, answering questions, and assisting with transactions around the clock. This ensures clients have access to support whenever they need it, without the delays of traditional service models.

A More Personalized Financial Experience

AI is redefining what personalized service looks like in finance. Instead of a one-size-fits-all approach, AI enables financial firms to tailor their recommendations to individual client needs. By analyzing spending habits, income patterns, and investment preferences, AI can help craft financial plans that align with specific goals, whether it’s retirement savings, wealth preservation, or long-term growth.

For clients working with financial advisors, AI serves as a powerful tool rather than a replacement. Advisors are using AI-driven insights to make more informed recommendations, offering strategies that are backed by real-time data rather than relying solely on historical trends. This results in more proactive wealth management, where adjustments can be made swiftly in response to market shifts.

Enhanced Security and Fraud Prevention

Financial security remains a top concern, and AI is playing a critical role in making transactions safer. Traditional fraud detection methods often relied on static rules that could miss evolving threats. AI, however, continuously learns from new patterns, allowing financial institutions to detect fraud before it happens.

Real-time monitoring ensures that even subtle changes in transaction behavior are analyzed for potential risks. If something appears out of the ordinary—such as an unusual withdrawal or login attempt—AI systems can flag the transaction for review or automatically take preventive action. This proactive approach gives clients greater peace of mind, knowing their financial assets are protected by cutting-edge technology.

AI’s Impact on Investment and Wealth Management

Investment strategies are becoming more sophisticated with AI-driven insights. By analyzing economic trends, market conditions, and historical data, AI can identify potential opportunities and risks with greater accuracy. This means clients receive smarter, data-backed recommendations that align with their financial goals.

Wealth management platforms powered by AI are also simplifying financial decision-making. Clients can access dynamic portfolio updates, risk assessments, and tailored investment suggestions without needing to spend hours analyzing data themselves. For those who prefer a hands-on approach, AI provides the insights they need to make informed decisions, while those who rely on financial advisors can be assured that their strategies are being continuously refined with real-time intelligence.

The Future of AI in Finance

As AI continues to evolve, its role in finance will only grow. The future will bring even more intelligent financial planning tools, enhanced fraud prevention, and hyper-personalized wealth management services. AI will not replace human advisors but will empower them with better tools, allowing for deeper, more data-driven client relationships.

Clients can expect financial firms to integrate AI in ways that enhance both security and efficiency. From automating everyday banking tasks to providing predictive insights that help navigate complex financial decisions, AI will continue to shape the future of wealth management. The firms that embrace these advancements will be better positioned to offer the highest level of service, ensuring clients receive smarter, safer, and more strategic financial guidance.

Conclusion

AI is revolutionizing financial services by making them more secure, personalized, and efficient. Whether it’s through advanced fraud detection, smarter investment strategies, or AI-powered financial planning, the benefits of AI-driven finance are becoming increasingly clear. Clients now have access to financial tools that were once only available to large institutions, leveling the playing field and allowing for more strategic wealth management.

The future of finance is one where AI and human expertise work hand in hand. As technology advances, clients will continue to see improvements in the way financial services are delivered—bringing greater security, better insights, and more opportunities to build and protect wealth.

by Cissy Blanchard | Mar 8, 2025 | Financial Planning

Over the last several weeks, President Trump’s White House and the Department of Government Efficiency (DOGE) have taken sweeping actions across the public sector in an effort to reduce the budget deficit and save U.S. taxpayers’ dollars. Meanwhile, Trump’s ongoing push-me-pull-you tariff debate has disrupted domestic and international markets, creating uncertainty for U.S. consumers and businesses. We’ll explore a variety of economic data points and policy initiatives that outline why we believe the markets think these efforts have a lot of bark – and not much bite.

Post-Election Returns Since 1948

Historically, equity markets tend to rally after a presidential election. The S&P 500 has risen by 4.7% since the 2024 election, outperforming the historical average post-election return of 1.7% observed during the post-World War II era. While there are always other external factors impacting financial markets beyond just elections, market participants should take comfort in this historical pattern.

S&P 500 Returns 75 Days Post-Election Since 1948

Source: Bloomberg, calculations by Horizon Investments, return is price return before the 1992 election and total return after, data as of market close on 02/25/2025. The S&P 500 or Standard & Poor’s 500 Index is a market-capitalization weighted index of the 500 largest U.S. publicly traded companies. Indices are unmanaged and do not have fees or expense charges, both of which would lower returns. It is not possible to invest directly in an unmanaged index.

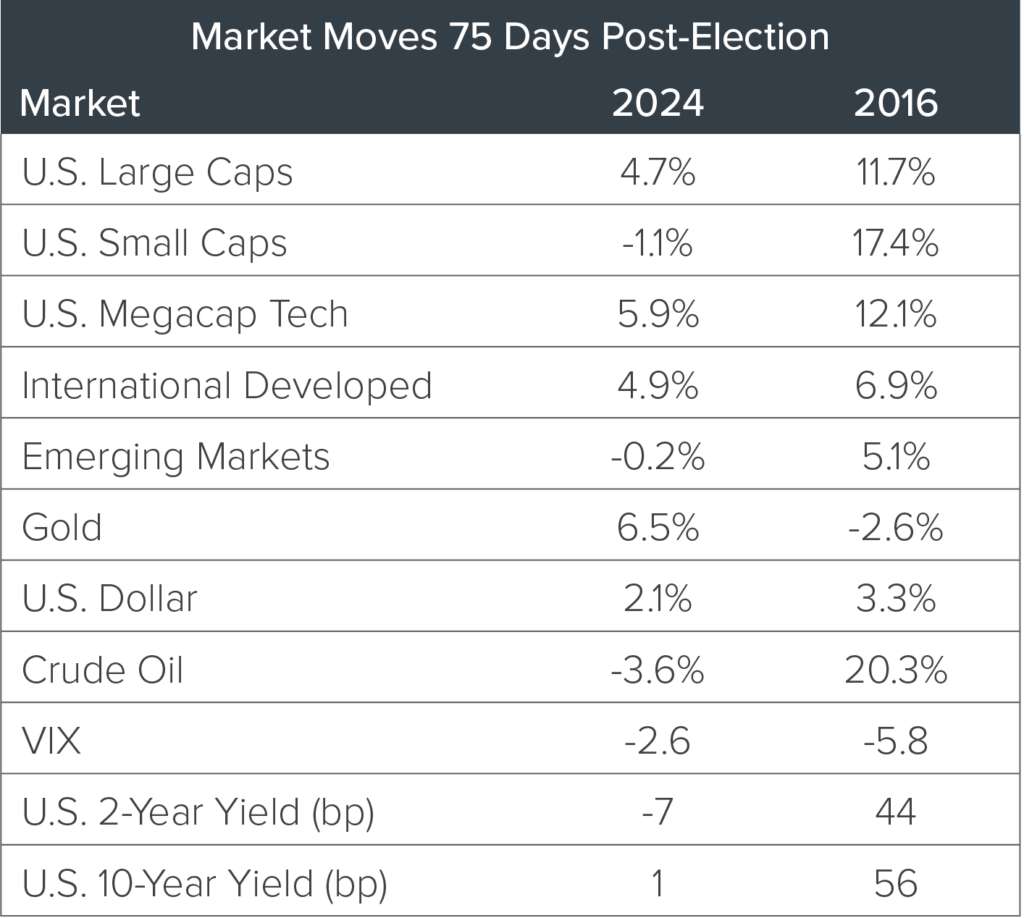

Cross-Asset Returns in 2024 vs. 2016

Many have highlighted market moves after Trump’s election in 2016 as a potential reference point for price action. We cautioned here against leaning too heavily on this framework, given the different starting points for markets and the economy compared with 2016.

Asset Class Performance Post-Election Day

Source: Bloomberg, data as of market close on November 4, 2024 through market close on February 25, 2025, and market close November 7, 2016 through market close on February 28th, 2017. Please see attached disclosures for information about these market sectors. Indices are unmanaged and do not have fees or expense charges, both of which would lower returns. It is not possible to invest directly in an unmanaged index.

A quick glance at the above chart reveals more differences than similarities between the market moves in reaction to Trump’s first and second election victory. Equity markets have generally seen a smaller bump this time, which is consistent with more demanding starting valuations and less of a policy surprise. The decline in small-caps and the muted reaction in crude oil stand out to us, likely indicators that the market is concerned about the negative growth impulse of potential tariff policy and lower fiscal spending, more prominent features of Trump’s agenda today. Similarly, U.S. Treasury yields have also seen more muted behavior than after the 2016 election. The lower move in equity volatility is one commonality between both elections, which we highlighted in our pre-election piece and will expand on below.

Post-Election Volatility

Since World War II, equity markets have, on average, been less volatile during the first year of a new presidential term compared to all other periods. These results may seem surprising, but they are repeating this year. Despite the flurry of activity in Washington, equity volatility (so far) has remained below both the post-election year average and the overall yearly average.

Realized Volatility During the First Year After an Election Since 1948

Source: Bloomberg, calculations by Horizon Investments, data as of market close on 02/25/2025.

Beyond easing fears after a major event like an election, there’s another special factor at play that’s helping to keep equity volatility low. Recently, individual stocks have been moving in divergent patterns – consider the difference between the AI-theme and the healthcare or banking sectors. This action tends to lower the volatility of the overall market. Environments like the current one may provide new opportunities as policies change and new trends emerge.

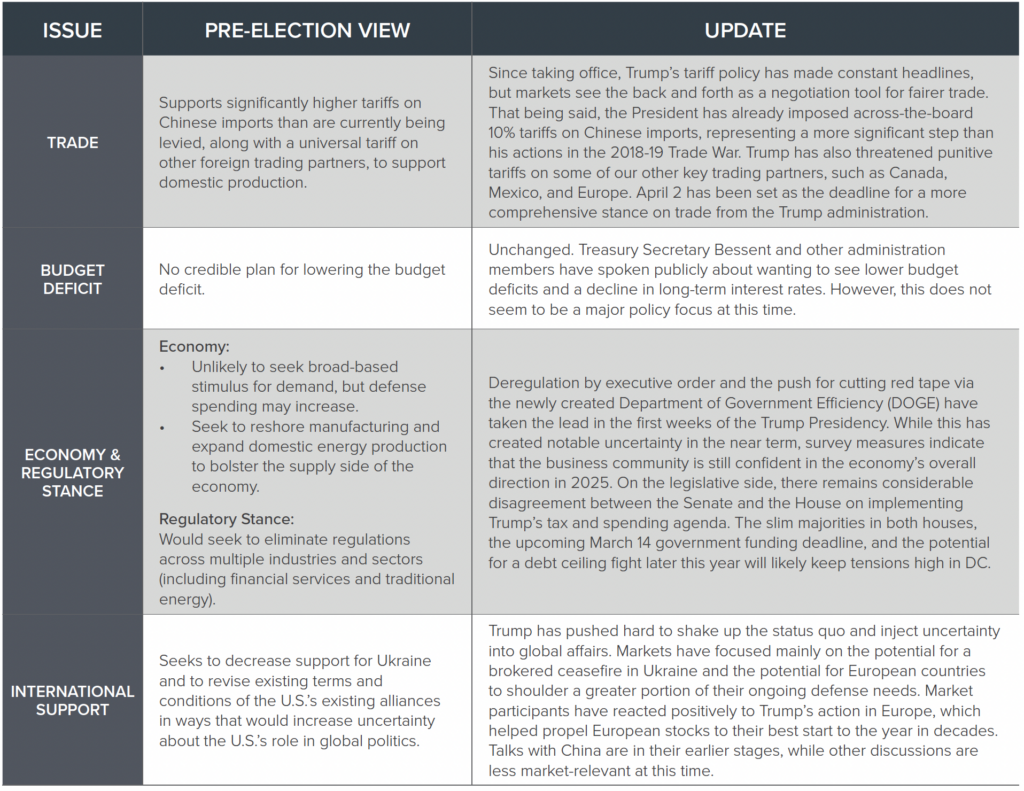

Update on President Trump’s Economic and Regulatory Initiatives

In our September pre-election piece, we highlighted several policy areas that we believed mattered to voters and markets. Below, we review five of these pre-election insights and compare them to what has happened since.

Conclusion

Today’s market landscape features a shifting balance between conflicting impulses: On the positive side, the rise in animal spirits in the business world and Trump’s deregulatory push support the economy and investor confidence. Against that, the potential business disruption of new trade policies and developments in the geopolitical arena creates unhelpful uncertainty. We expect this back and forth to uncover potential investment opportunities in the months ahead.

Taking a broader view, two points stand out to us from reviewing the above data, as well as the market price action and newsflow of the past months:

- Don’t freak out: Uncertainty and change may seem scary in the near term, but the data suggests making rash portfolio changes in such an environment is not conducive to long-term success.

- Don’t trade on politics: Translating political actions into market prices is rarely a straightforward exercise, and that’s before one even considers the potential for bias to enter the equation. Encouraging your clients to focus on the bigger picture can help them stay on the right track.

Instead, stay the course.

As we have long stated, other things matter more to markets than politics. By focusing on risk management and growth potential, you can help your clients’ portfolios remain aligned with their long-term financial goals.

To Read Original Article Click Here

by Cissy Blanchard | Mar 4, 2025 | Financial Planning

For generations, wealthy families have been told that keeping assets together preserves legacy and unity. But as families grow, so do differences in priorities, risk tolerance, and financial goals.

What if the best way to protect family wealth isn’t keeping it together—but dividing it strategically?

Rather than being a last resort, asset division can be a proactive solution that empowers each family branch, reduces unnecessary tension, and ultimately leads to greater financial success.

The Hidden Risks of Pooled Family Wealth

Pooling assets might seem like the simplest way to maintain harmony, but it often creates more complexity than clarity. Families navigating shared businesses, investments, or trusts frequently face these challenges:

- Conflicting Priorities – One generation may prioritize financial security, while another seeks high-growth opportunities.

- Strained Decision-Making – More stakeholders mean slower decisions and increased friction.

- Unbalanced Contributions – Some members may be more actively involved in managing wealth, while others passively benefit.

- Limited Flexibility – A single structure leaves little room for personal financial goals or customized investment strategies.

Instead of forcing every family member into the same financial mold, separating assets strategically can offer autonomy without sacrificing unity.

Why Dividing Assets Can Strengthen Family Wealth

Separating assets isn’t about breaking up the family—it’s about ensuring that everyone has the freedom to make financial decisions that align with their goals.

1. Business Growth Without Conflict

Many family businesses struggle to transition from one generation to the next. Instead of fighting over leadership roles, separating business divisions or selling off certain assets allows different family members to focus on what they do best.

For example, a family that owns a retail empire might find that some members are passionate about e-commerce, while others prefer real estate holdings. Splitting these interests ensures each person is working toward their strengths—without unnecessary disputes.

2. Customized Investment Strategies

Not every family member has the same risk tolerance. Some may prefer conservative, income-generating investments, while others lean toward aggressive growth strategies.

Dividing investment assets into separate portfolios allows each branch of the family to manage their funds according to their unique goals, avoiding frustration over differing financial philosophies.

3. Personalized Philanthropy That Reflects Individual Values

Philanthropy is deeply personal. While some families prefer to give collectively, others find that having separate charitable funds enables each member to support causes they truly care about—without pressure to conform to a single mission.

A structured approach, such as individual donor-advised funds or personal philanthropic trusts, allows family members to contribute to their chosen causes while still aligning with the overall family legacy.

4. Reduced Estate Conflicts

One of the biggest sources of tension in family wealth planning is inheritance disputes. When multiple heirs are expected to share ownership of assets, disagreements over management and distribution can quickly arise.

By creating separate trusts or asset divisions early, families can ensure that each member receives their portion in a way that minimizes disputes and maximizes financial security.

How to Structure Asset Division Without Causing Friction

While dividing assets can be beneficial, it needs to be done thoughtfully to avoid unintended consequences. Here’s how families can create a structured, conflict-free approach:

1. Establish Clear Governance Structures

Setting clear guidelines on how assets will be separated and managed prevents future misunderstandings. This can include:

- Defining individual ownership rights

- Outlining decision-making processes

- Creating buyout options for shared assets

2. Communicate Early and Often

Transparency is key when restructuring family wealth. Holding family meetings to discuss financial structures, personal goals, and potential concerns ensures that all voices are heard.

3. Work with Financial and Legal Experts

Separating assets effectively requires careful tax planning, legal structuring, and financial expertise. An experienced advisory team can help families navigate complex decisions while ensuring wealth is preserved across generations.

Final Thought: Strength Through Independence

Preserving family wealth doesn’t have to mean keeping everything together. In fact, strategically dividing assets can provide the flexibility, autonomy, and clarity that families need to thrive.

By embracing a more customized approach to wealth management, families can empower each generation to make financial decisions that align with their vision—without unnecessary conflict.

After all, true legacy isn’t about how wealth is structured—it’s about how well it supports the future.

by Cissy Blanchard | Feb 18, 2025 | Financial Planning

Understanding Financial Aid: A Key to Education Success

Education expenses can be a significant burden for families and students. Whether you’re saving for a child’s future or financing your own education, understanding financial aid is essential. National Financial Aid Awareness Month provides the perfect opportunity to explore how financial aid can ease the cost of education and become an integral part of your broader financial strategy.

The Role of Financial Aid in Education Planning

Financial aid helps students and families cover the increasing costs of education, from tuition to housing and supplies. Understanding the available financial aid options can make education more accessible and manageable.

Types of Financial Aid Available

- Grants and Scholarships – These awards don’t require repayment and are typically based on merit or financial need.

- Federal Loans – Government-backed loans offer lower interest rates and flexible repayment options.

- Work-Study Programs – Students can earn money while gaining work experience through on-campus or approved part-time jobs.

- Private Loans – While these can supplement federal aid, they come with varying interest rates and terms, requiring careful evaluation.

For students, understanding these options empowers them to make informed financial decisions. For parents, integrating financial aid into their education planning ensures their children have resources without sacrificing other financial goals.

Integrating Financial Aid into a Broader Financial Plan

While financial aid is valuable, it’s only one piece of a well-rounded financial strategy. To maintain financial stability while funding education, consider these key areas:

1. Budgeting for Education Costs

- Students should learn to live within their means by tracking education-related expenses.

- Parents need to balance education costs with everyday family expenses.

2. Education Savings Plans

- 529 Plans & Education Savings Accounts (ESAs) offer tax-advantaged ways to save for future education expenses.

3. Investing for Long-Term Growth

- Investments can complement education savings and help grow financial resources over time.

4. Balancing Education with Retirement Planning

- Avoid prioritizing college savings over retirement. A balanced strategy ensures long-term financial security.

Actionable Tips to Maximize Financial Aid Opportunities

1. Submit the FAFSA Early

The Free Application for Federal Student Aid (FAFSA) is the foundation of financial aid. Apply as early as possible to maximize eligibility.

2. Research Scholarships and Grants

Many organizations offer scholarships based on academics, extracurricular activities, and demographics. Invest time in finding opportunities that fit your profile.

3. Plan for Total College Expenses

Consider hidden costs like books, supplies, transportation, and housing when estimating education expenses.

4. Explore Work-Study Programs

These opportunities provide financial assistance and real-world experience to help students gain valuable skills.

5. Avoid Over-Borrowing

Only borrow what’s necessary to prevent unnecessary financial stress after graduation.

Reassess Your Financial Plan This Financial Aid Awareness Month

National Financial Aid Awareness Month is the perfect time to reflect on your financial planning:

Are you saving enough for education?

Are your retirement and financial goals on track?

Have your financial priorities shifted recently?

A holistic financial plan ensures that all elements—education, savings, and retirement—work together harmoniously.

Seek Professional Guidance

A financial advisor can help:

✔ Align education savings with other financial priorities.

✔ Explore tax-efficient ways to save for college.

✔ Evaluate loan repayment strategies.

✔ Develop a comprehensive financial strategy tailored to your family’s needs.

Take the First Step Toward Financial Confidence

Financial aid is a powerful tool, but it’s most effective when paired with a solid financial plan. This National Financial Aid Awareness Month, take action by learning about financial aid options and incorporating them into your overall financial strategy.

Ready to create a customized plan? Contact us today for a personalized consultation and take control of your financial future.

Recent Comments